Running A Backtest¶

In this example we will demonstrate how to run a backtest for a simple algo example

Loading the data bundle¶

[95]:

import os

import warnings

warnings.filterwarnings('ignore')

os.environ['ZIPLINE_ROOT'] = os.path.join(os.getcwd(), '.zipline')

os.listdir(os.environ['ZIPLINE_ROOT'])

os.environ['ZIPLINE_TRADER_CONFIG'] = os.path.join(os.getcwd(), "./zipline-trader.yaml")

with open(os.environ['ZIPLINE_TRADER_CONFIG'], 'r') as f:

data = f.read()

print(data[:20])

import zipline

from zipline.data import bundles

bundle_name = 'alpaca_api'

bundle_data = bundles.load(bundle_name)

from zipline.pipeline.loaders import USEquityPricingLoader

from zipline.utils.calendars import get_calendar

from zipline.pipeline.data import USEquityPricing

from zipline.data.data_portal import DataPortal

import pandas as pd

# Set the dataloader

pricing_loader = USEquityPricingLoader.without_fx(bundle_data.equity_daily_bar_reader, bundle_data.adjustment_reader)

# Define the function for the get_loader parameter

def choose_loader(column):

if column not in USEquityPricing.columns:

raise Exception('Column not in USEquityPricing')

return pricing_loader

# Set the trading calendar

trading_calendar = get_calendar('NYSE')

start_date = pd.Timestamp('2019-07-05', tz='utc')

end_date = pd.Timestamp('2020-11-13', tz='utc')

# Create a data portal

data_portal = DataPortal(bundle_data.asset_finder,

trading_calendar = trading_calendar,

first_trading_day = start_date,

equity_daily_reader = bundle_data.equity_daily_bar_reader,

adjustment_reader = bundle_data.adjustment_reader)

[96]:

import dateutil.parser

from os.path import join, exists

import pandas as pd

import pandas_datareader.data as yahoo_reader

import yaml

import numpy as np

def get_benchmark(symbol=None, start = None, end = None, other_file_path=None):

bm = yahoo_reader.DataReader(symbol,

'yahoo',

pd.Timestamp(start),

pd.Timestamp(end))['Close']

bm.index = bm.index.tz_localize('UTC')

return bm.pct_change(periods=1).fillna(0)

[97]:

from zipline.api import order_target, record, symbol

import matplotlib.pyplot as plt

def initialize(context):

context.equity = bundle_data.asset_finder.lookup_symbol("AMZN", end_date)

def handle_data(context, data):

order_target(context.equity, 100)

def before_trading_start(context, data):

pass

def analyze(context, perf):

ax1 = plt.subplot(211)

perf.portfolio_value.plot(ax=ax1)

ax2 = plt.subplot(212, sharex=ax1)

perf.sym.plot(ax=ax2, color='r')

plt.gcf().set_size_inches(18, 8)

plt.legend(['Algo', 'Benchmark'])

plt.ylabel("Returns", color='black', size=25)

[98]:

import pandas as pd

from datetime import datetime

import pytz

from zipline import run_algorithm

start = pd.Timestamp(datetime(2020, 1, 1, tzinfo=pytz.UTC))

end = pd.Timestamp(datetime(2020, 11, 1, tzinfo=pytz.UTC))

r = run_algorithm(start=start,

end=end,

initialize=initialize,

capital_base=100000,

handle_data=handle_data,

benchmark_returns=get_benchmark(symbol="SPY",

start=start.date().isoformat(),

end=end.date().isoformat()),

bundle='alpaca_api',

broker=None,

state_filename="./demo.state",

trading_calendar=trading_calendar,

before_trading_start=before_trading_start,

# analyze=analyze,

data_frequency='daily'

)

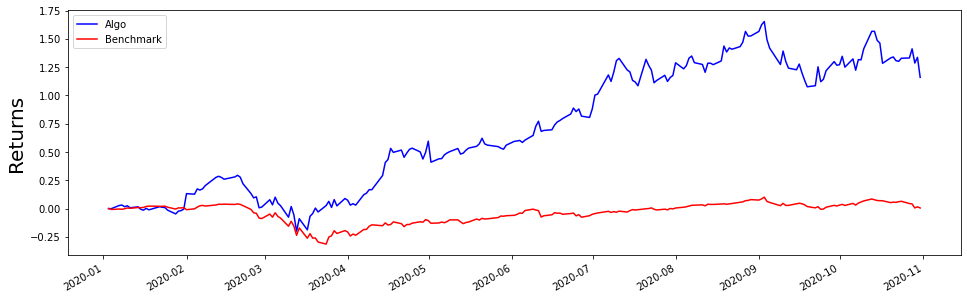

fig, axes = plt.subplots(1, 1, figsize=(16, 5), sharex=True)

r.algorithm_period_return.plot(color='blue')

r.benchmark_period_return.plot(color='red')

plt.legend(['Algo', 'Benchmark'])

plt.ylabel("Returns", color='black', size=20)

[98]:

Text(0, 0.5, 'Returns')

Using Pyfolio to analyze your results¶

[99]:

import pyfolio as pf

returns, positions, transactions = pf.utils.extract_rets_pos_txn_from_zipline(r)

benchmark_returns = r.benchmark_period_return

[100]:

import empyrical

print("returns sharp ratio: {}".format(empyrical.sharpe_ratio(returns))) # how much is it sensative to divergance. the higher the better

print("bencmark sharp ratio: {}".format(empyrical.sharpe_ratio(benchmark_returns)))

print("beta ratio: {}".format(empyrical.beta(returns, benchmark_returns))) # how much correlation between algo to benchmark. we want it to be clsoe to zero

print("alpha ratio: {}".format(empyrical.alpha(returns, benchmark_returns)))

returns sharp ratio: 1.7147226500268884

bencmark sharp ratio: -6.584559370521319

beta ratio: -0.010817530431739008

alpha ratio: 1.829456229577063

[101]:

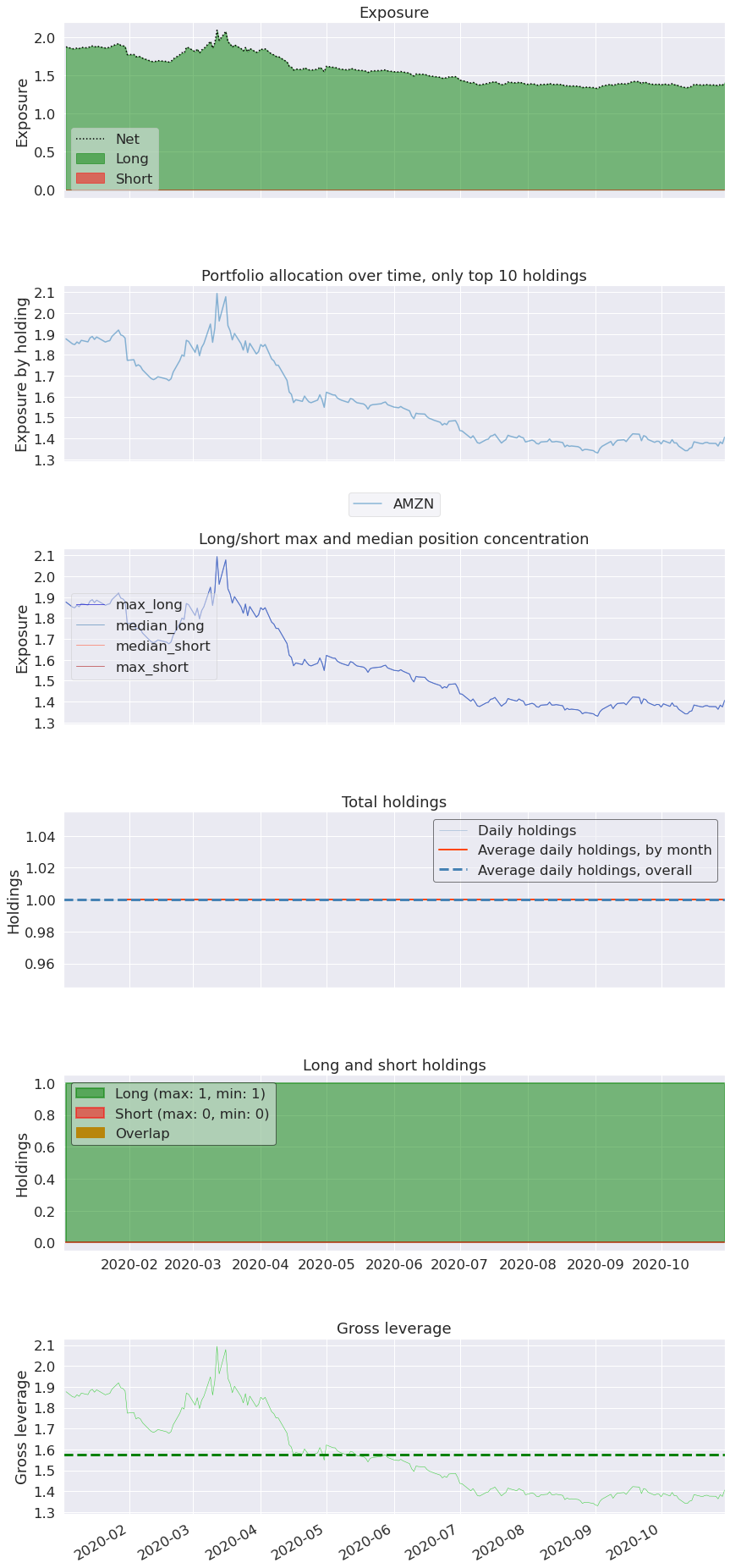

pf.create_position_tear_sheet(returns, positions=positions, transactions=transactions)

| Top 10 long positions of all time | max |

|---|---|

| sid | |

| AMZN | 209.44% |

| Top 10 short positions of all time | max |

|---|---|

| sid |

| Top 10 positions of all time | max |

|---|---|

| sid | |

| AMZN | 209.44% |

[102]:

pf.create_returns_tear_sheet(returns,

positions=positions,

transactions=transactions,

benchmark_rets=benchmark_returns)

| Start date | 2020-01-02 | |

|---|---|---|

| End date | 2020-10-30 | |

| Total months | 10 | |

| Backtest | ||

| Annual return | 150.903% | |

| Cumulative returns | 116.026% | |

| Annual volatility | 66.542% | |

| Sharpe ratio | 1.71 | |

| Calmar ratio | 3.95 | |

| Stability | 0.87 | |

| Max drawdown | -38.166% | |

| Omega ratio | 1.35 | |

| Sortino ratio | 2.67 | |

| Skew | 0.13 | |

| Kurtosis | 1.98 | |

| Tail ratio | 1.17 | |

| Daily value at risk | -7.931% | |

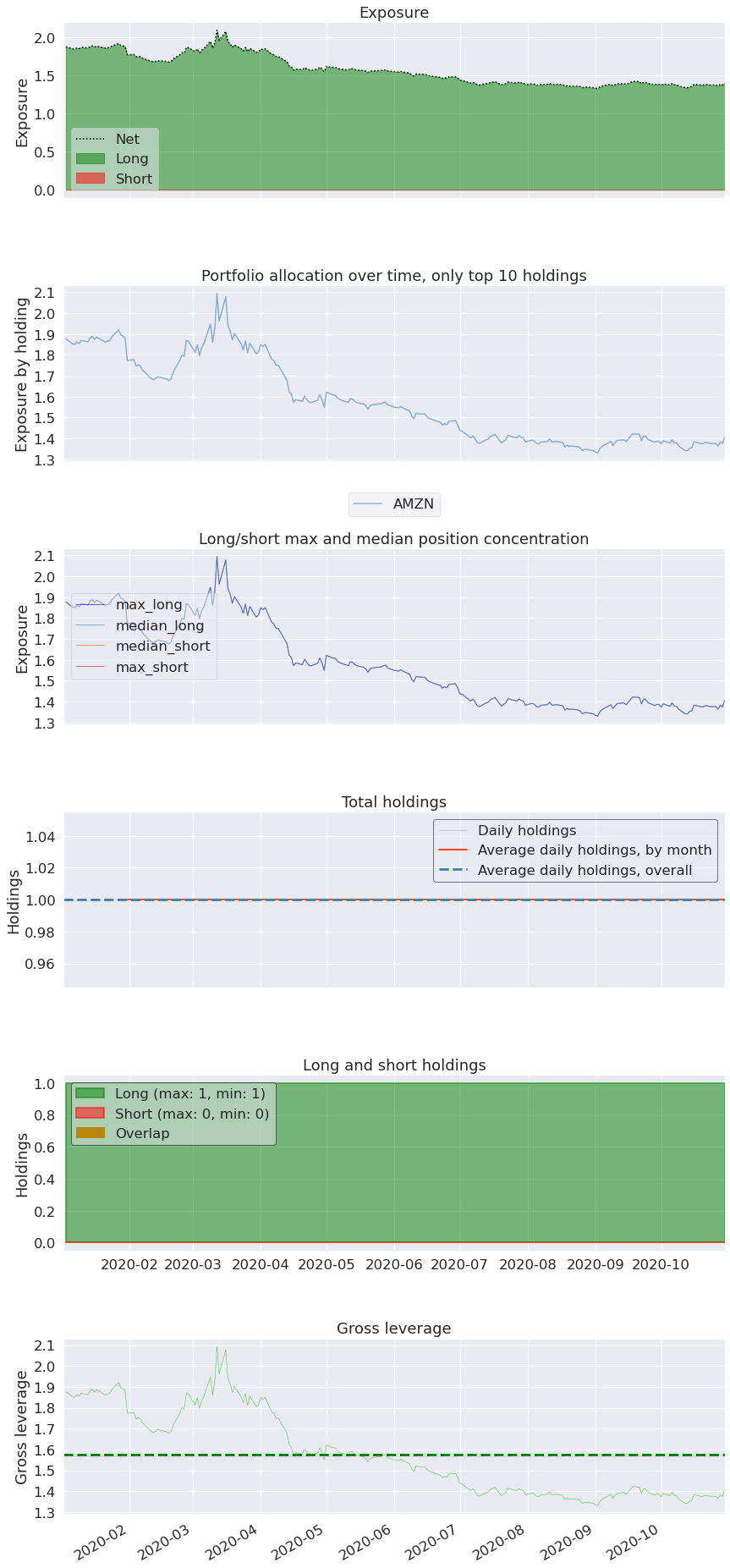

| Gross leverage | 1.57 | |

| Daily turnover | 0.953% | |

| Alpha | 1.83 | |

| Beta | -0.01 | |

| Worst drawdown periods | Net drawdown in % | Peak date | Valley date | Recovery date | Duration |

|---|---|---|---|---|---|

| 0 | 38.17 | 2020-02-19 | 2020-03-12 | 2020-04-14 | 40 |

| 1 | 21.73 | 2020-09-02 | 2020-09-18 | NaT | NaN |

| 2 | 11.63 | 2020-04-30 | 2020-05-01 | 2020-05-20 | 15 |

| 3 | 10.39 | 2020-07-10 | 2020-07-17 | 2020-08-05 | 19 |

| 4 | 7.56 | 2020-01-07 | 2020-01-27 | 2020-01-31 | 19 |

[103]:

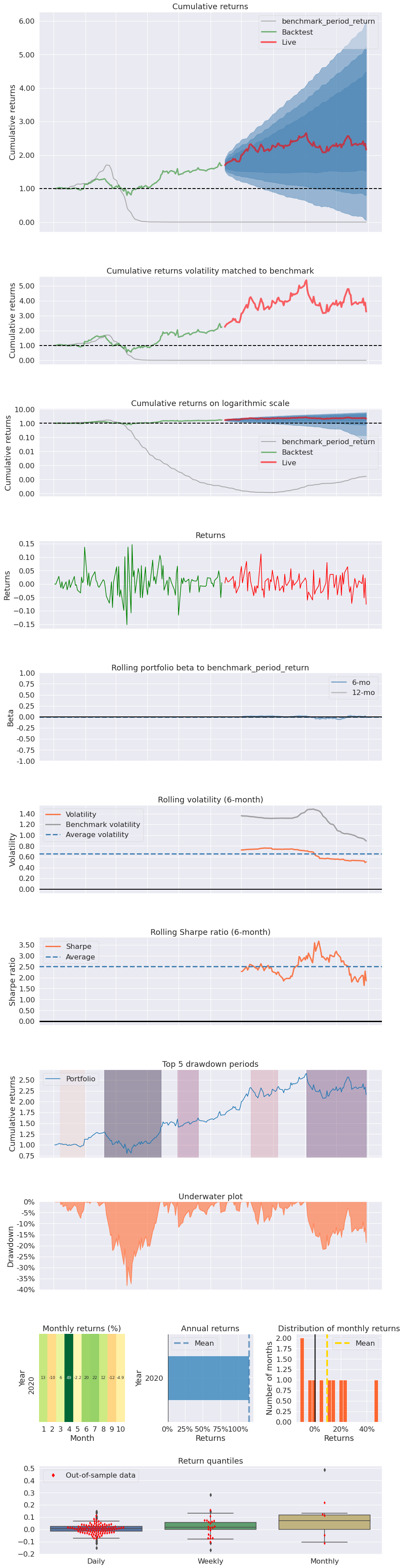

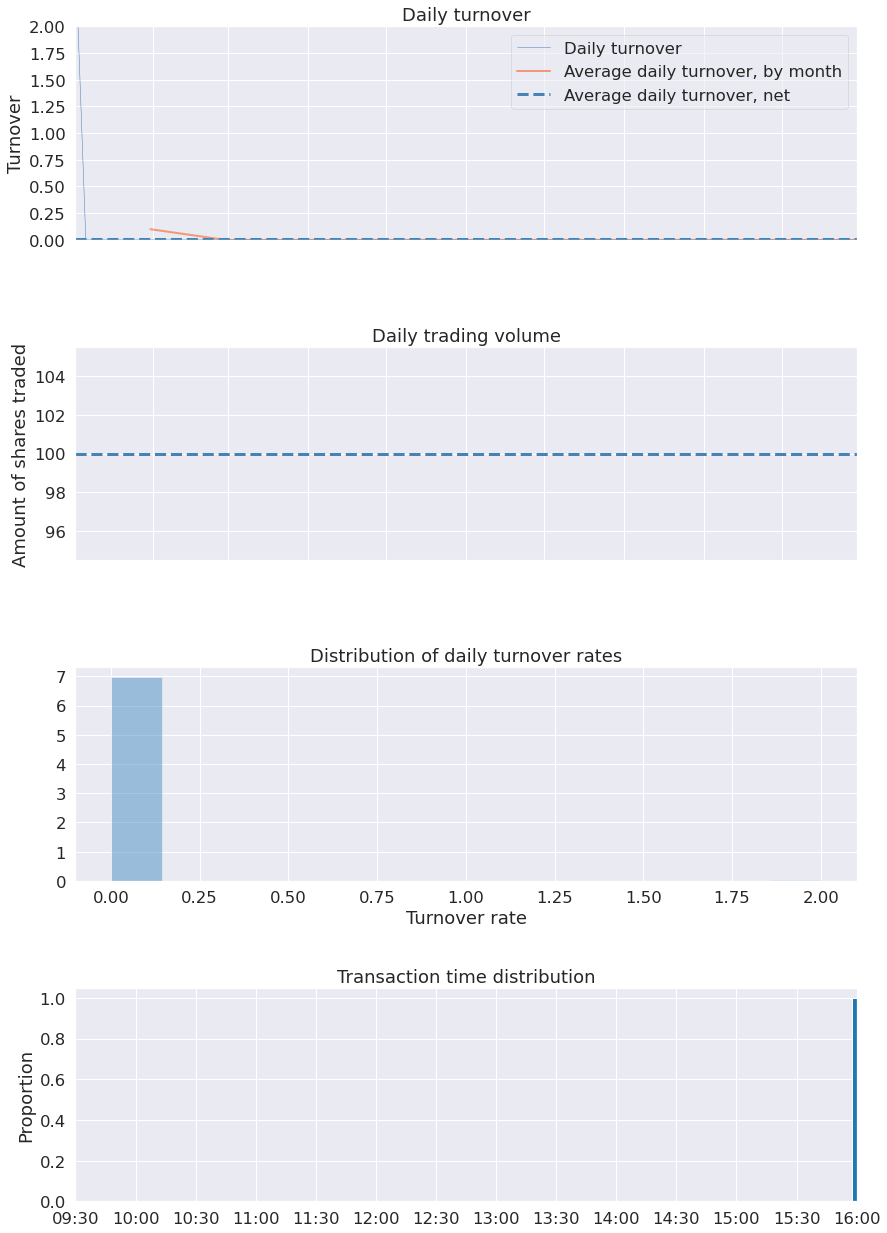

pf.create_full_tear_sheet(returns,

positions=positions,

transactions=transactions,

live_start_date="2020-06-13",

round_trips=True,

benchmark_rets=benchmark_returns)

| Start date | 2020-01-02 | |||

|---|---|---|---|---|

| End date | 2020-10-30 | |||

| In-sample months | 5 | |||

| Out-of-sample months | 4 | |||

| All | In-sample | Out-of-sample | ||

| Annual return | 150.903% | 222.617% | 87.764% | |

| Cumulative returns | 116.026% | 69.084% | 27.763% | |

| Annual volatility | 66.542% | 75.493% | 54.733% | |

| Sharpe ratio | 1.71 | 1.93 | 1.42 | |

| Calmar ratio | 3.95 | 5.83 | 4.04 | |

| Stability | 0.87 | 0.63 | 0.40 | |

| Max drawdown | -38.166% | -38.166% | -21.734% | |

| Omega ratio | 1.35 | 1.42 | 1.26 | |

| Sortino ratio | 2.67 | 3.01 | 2.22 | |

| Skew | 0.13 | 0.05 | 0.23 | |

| Kurtosis | 1.98 | 1.85 | 0.37 | |

| Tail ratio | 1.17 | 1.24 | 1.10 | |

| Daily value at risk | -7.931% | -8.933% | -6.587% | |

| Gross leverage | 1.57 | 1.73 | 1.40 | |

| Daily turnover | 0.953% | 1.787% | 0.0% | |

| Alpha | 1.83 | 3.35 | 1.42 | |

| Beta | -0.01 | 0.00 | -0.02 | |

| Worst drawdown periods | Net drawdown in % | Peak date | Valley date | Recovery date | Duration |

|---|---|---|---|---|---|

| 0 | 38.17 | 2020-02-19 | 2020-03-12 | 2020-04-14 | 40 |

| 1 | 21.73 | 2020-09-02 | 2020-09-18 | NaT | NaN |

| 2 | 11.63 | 2020-04-30 | 2020-05-01 | 2020-05-20 | 15 |

| 3 | 10.39 | 2020-07-10 | 2020-07-17 | 2020-08-05 | 19 |

| 4 | 7.56 | 2020-01-07 | 2020-01-27 | 2020-01-31 | 19 |

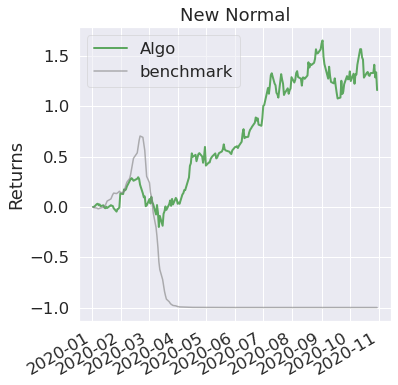

| Stress Events | mean | min | max |

|---|---|---|---|

| New Normal | 0.45% | -15.20% | 14.70% |

| Top 10 long positions of all time | max |

|---|---|

| sid | |

| AMZN | 209.44% |

| Top 10 short positions of all time | max |

|---|---|

| sid |

| Top 10 positions of all time | max |

|---|---|

| sid | |

| AMZN | 209.44% |