Using Alphalens¶

In this example we will demonstrate how to create a simple pipeline that uses a factor and then analyze it using alphalens.

Loading the data bundle¶

[2]:

import warnings

warnings.filterwarnings('ignore')

import os

import pandas as pd

from datetime import timedelta

os.environ['ZIPLINE_ROOT'] = os.path.join(os.getcwd(), '.zipline')

os.listdir(os.environ['ZIPLINE_ROOT'])

os.environ['ZIPLINE_TRADER_CONFIG'] = os.path.join(os.getcwd(), "./zipline-trader.yaml")

with open(os.environ['ZIPLINE_TRADER_CONFIG'], 'r') as f:

data = f.read()

print(data[:20])

import zipline

from zipline.data import bundles

from zipline.utils.calendars import get_calendar

from zipline.pipeline.data import USEquityPricing

from zipline.pipeline.factors import CustomFactor

from zipline.research.utils import get_pricing, create_data_portal, create_pipeline_engine

# Set the trading calendar

trading_calendar = get_calendar('NYSE')

bundle_name = 'alpaca_api'

start_date = pd.Timestamp('2015-12-31', tz='utc')

pipeline_start_date = start_date + timedelta(days=365*2+10)

end_date = pd.Timestamp('2020-12-28', tz='utc')

data_portal = create_data_portal(bundle_name, trading_calendar, start_date)

Creating the Pipeline Engine¶

[3]:

engine = create_pipeline_engine(bundle_name)

Let’s create our custom factor¶

This is a factor that runs a linear regression over one year of stock log returns and calculates a “slope” as our factor.

[4]:

from zipline.pipeline.factors import CustomFactor, Returns

from zipline.pipeline.data import USEquityPricing

class YearlyReturns(CustomFactor):

inputs = [USEquityPricing.close]

window_length = 252

def compute(self, today, assets, out, prices):

start = self.window_length

out[:] = (prices[-1] - prices[-start])/prices[-start]

Our Pipeline¶

[7]:

from zipline.pipeline.domain import US_EQUITIES

from zipline.pipeline.factors import AverageDollarVolume

from zipline.pipeline import Pipeline

from zipline.pipeline.classifiers.custom.sector import ZiplineTraderSector, SECTOR_LABELS

universe = USEquityPricing

universe = AverageDollarVolume(window_length = 5)

pipeline = Pipeline(

columns = {

'MyFactor' : YearlyReturns(),

# 'Returns': Returns(window_length=252), # same as YearlyRetruns

'Sector' : ZiplineTraderSector()

}, domain=US_EQUITIES

)

Run the Pipeline¶

[8]:

# Run our pipeline for the given start and end dates

factors = engine.run_pipeline(pipeline, pipeline_start_date, end_date)

factors.head()

[8]:

| MyFactor | Sector | ||

|---|---|---|---|

| 2018-01-09 00:00:00+00:00 | Equity(0 [A]) | 0.455036 | 1 |

| Equity(1 [AAL]) | 0.118720 | 11 | |

| Equity(2 [ABC]) | 0.133466 | 7 | |

| Equity(3 [ABMD]) | 0.774400 | 7 | |

| Equity(4 [ADP]) | 0.150161 | 10 |

Data preparation¶

Alphalens input consists of two type of information: the factor values for the time period under analysis and the historical assets prices (or returns). Alphalens doesn’t need to know how the factor was computed, the historical factor values are enough. This is interesting because we can use the tool to evaluate factors for which we have the data but not the implementation details.

Alphalens requires that factor and price data follows a specific format and it provides an utility function, get_clean_factor_and_forward_returns, that accepts factor data, price data and optionally a group information (for example the sector groups, useful to perform sector specific analysis) and returns the data suitably formatted for Alphalens.

[9]:

asset_list = factors.index.levels[1].unique()

prices = get_pricing(

data_portal,

trading_calendar,

asset_list,

pipeline_start_date,

end_date)

prices.head()

[9]:

| Equity(0 [A]) | Equity(1 [AAL]) | Equity(2 [ABC]) | Equity(3 [ABMD]) | Equity(4 [ADP]) | Equity(5 [AEE]) | Equity(6 [AES]) | Equity(7 [AJG]) | Equity(8 [ALB]) | Equity(9 [ALK]) | ... | Equity(495 [TWTR]) | Equity(496 [UNM]) | Equity(497 [UNP]) | Equity(498 [UPS]) | Equity(499 [VMC]) | Equity(500 [VRSK]) | Equity(501 [VZ]) | Equity(502 [WBA]) | Equity(503 [WEC]) | Equity(504 [ZTS]) | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2018-01-10 00:00:00+00:00 | 70.80 | 53.78 | 97.20 | 208.21 | 117.66 | 56.49 | 10.775 | 63.575 | 132.96 | 72.07 | ... | 24.240 | 57.520 | 139.71 | 129.77 | 132.39 | 96.32 | 51.69 | 74.06 | 63.68 | 73.90 |

| 2018-01-11 00:00:00+00:00 | 70.80 | 56.18 | 98.12 | 210.17 | 117.18 | 56.15 | 10.960 | 63.390 | 134.68 | 74.82 | ... | 24.340 | 58.210 | 140.40 | 133.46 | 135.18 | 96.67 | 52.12 | 75.36 | 63.58 | 74.60 |

| 2018-01-12 00:00:00+00:00 | 71.72 | 58.22 | 98.99 | 215.19 | 118.39 | 55.50 | 11.030 | 63.875 | 133.46 | 73.52 | ... | 25.415 | 58.600 | 141.17 | 134.08 | 133.97 | 97.48 | 51.87 | 76.03 | 63.63 | 75.40 |

| 2018-01-16 00:00:00+00:00 | 71.24 | 57.73 | 99.55 | 218.27 | 119.38 | 55.45 | 10.680 | 63.410 | 128.00 | 71.28 | ... | 24.680 | 55.530 | 140.30 | 132.90 | 133.67 | 97.19 | 51.66 | 76.03 | 63.15 | 75.55 |

| 2018-01-17 00:00:00+00:00 | 72.05 | 57.91 | 101.29 | 224.23 | 122.05 | 55.79 | 10.730 | 64.040 | 126.96 | 70.83 | ... | 24.550 | 56.355 | 140.46 | 134.01 | 134.58 | 98.01 | 51.73 | 75.78 | 63.56 | 76.76 |

5 rows × 505 columns

[10]:

import alphalens as al

[11]:

factor_data = al.utils.get_clean_factor_and_forward_returns(

factor=factors["MyFactor"],

prices=prices,

quantiles=5,

periods=[1, 5, 10],

groupby=factors["Sector"],

binning_by_group=True,

groupby_labels=SECTOR_LABELS,

max_loss=0.8)

Dropped 1.5% entries from factor data: 1.5% in forward returns computation and 0.0% in binning phase (set max_loss=0 to see potentially suppressed Exceptions).

max_loss is 80.0%, not exceeded: OK!

[12]:

factor_data.head(10)

[12]:

| 1D | 5D | 10D | factor | group | factor_quantile | ||

|---|---|---|---|---|---|---|---|

| date | asset | ||||||

| 2018-01-10 00:00:00+00:00 | Equity(0 [A]) | 0.000000 | 0.019492 | 0.043079 | 0.491687 | Capital Goods | 4 |

| Equity(1 [AAL]) | 0.044626 | 0.080141 | -0.017851 | 0.085696 | Transportation | 2 | |

| Equity(2 [ABC]) | 0.009465 | 0.037757 | 0.073765 | 0.149593 | Health Care | 3 | |

| Equity(3 [ABMD]) | 0.009414 | 0.084914 | 0.135200 | 0.868852 | Health Care | 5 | |

| Equity(4 [ADP]) | -0.004080 | 0.027707 | 0.025497 | 0.162133 | Technology | 1 | |

| Equity(5 [AEE]) | -0.006019 | -0.019295 | 0.004780 | 0.102944 | Public Utilities | 3 | |

| Equity(6 [AES]) | 0.017169 | 0.070070 | 0.067285 | -0.050309 | Basic Industries | 1 | |

| Equity(7 [AJG]) | -0.002910 | 0.007000 | 0.032796 | 0.213659 | Finance | 3 | |

| Equity(8 [ALB]) | 0.012936 | -0.113147 | -0.120751 | 0.507343 | Basic Industries | 5 | |

| Equity(9 [ALK]) | 0.038157 | -0.031636 | -0.138754 | -0.225000 | Transportation | 1 |

Running Alphalens¶

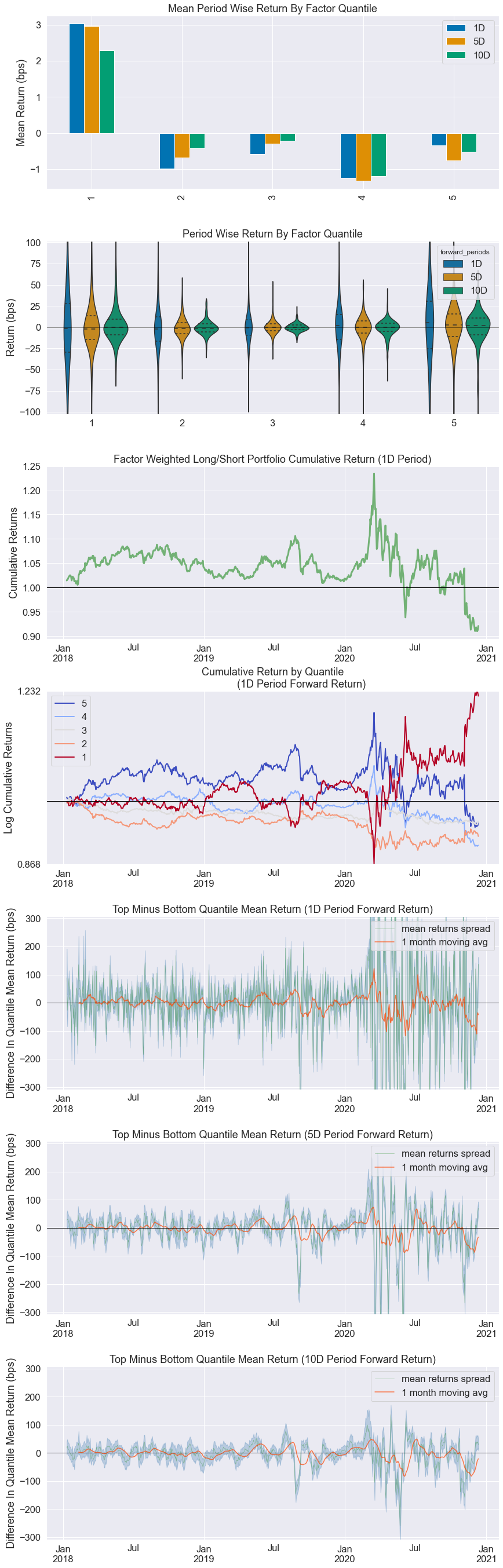

Once the factor data is ready, running Alphalens analysis is pretty simple and it consists of one function call that generates the factor report (statistical information and plots). Please remember that it is possible to use the help python built-in function to view the details of a function.

[13]:

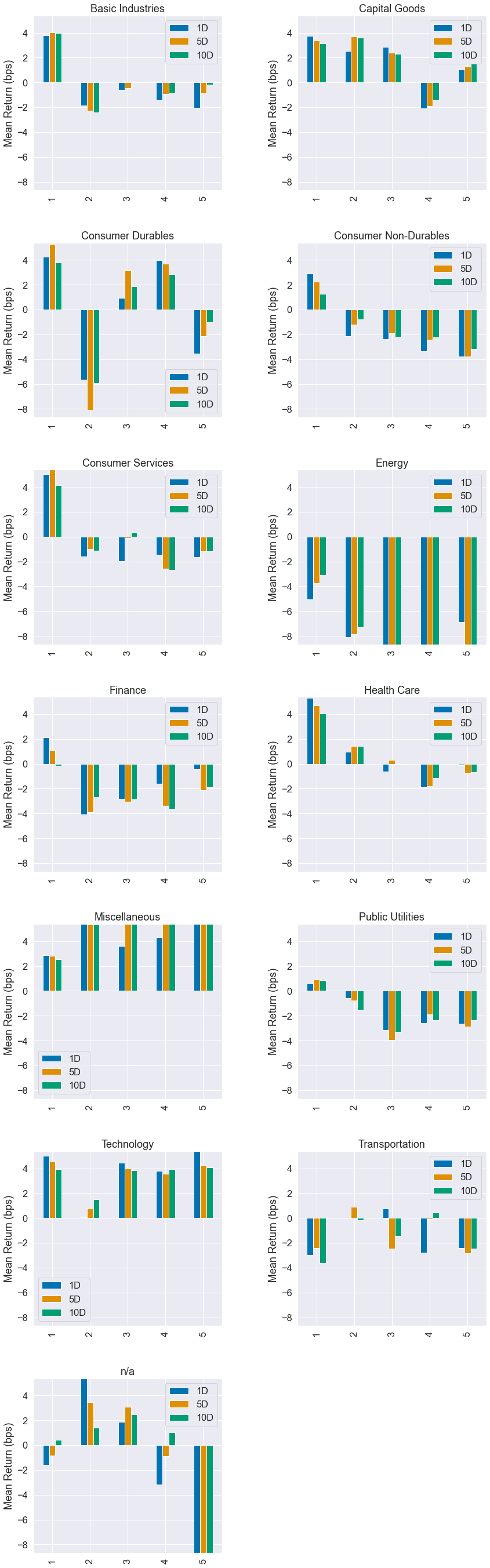

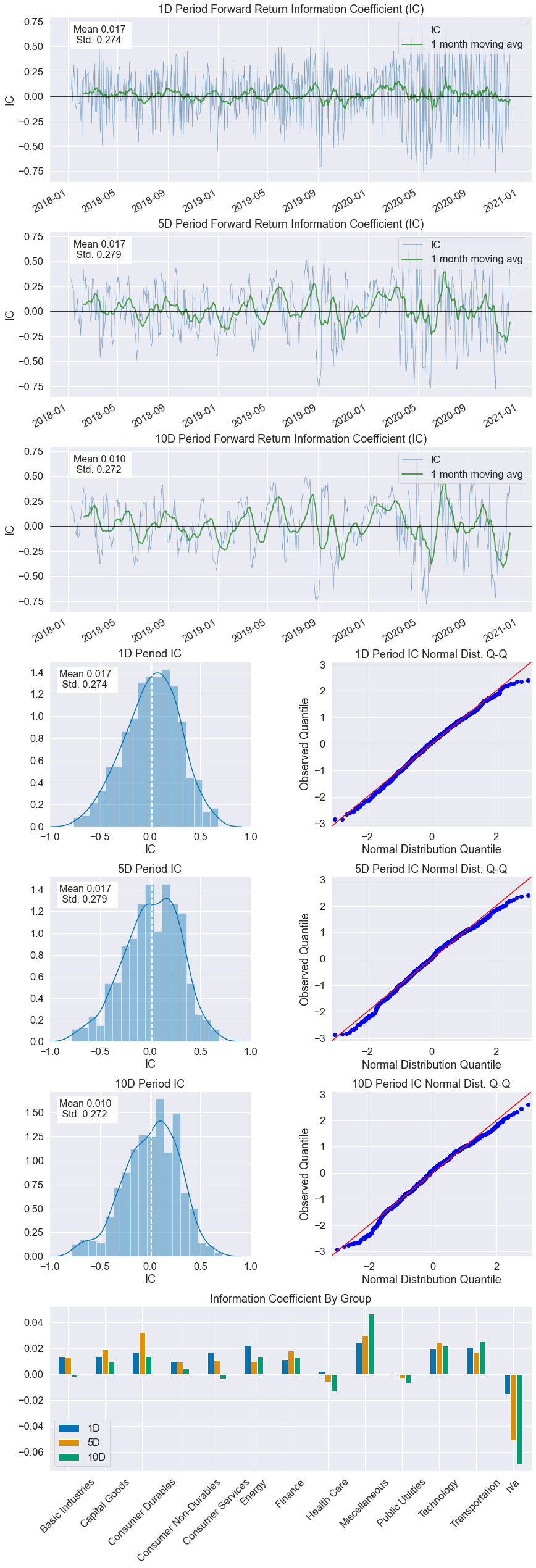

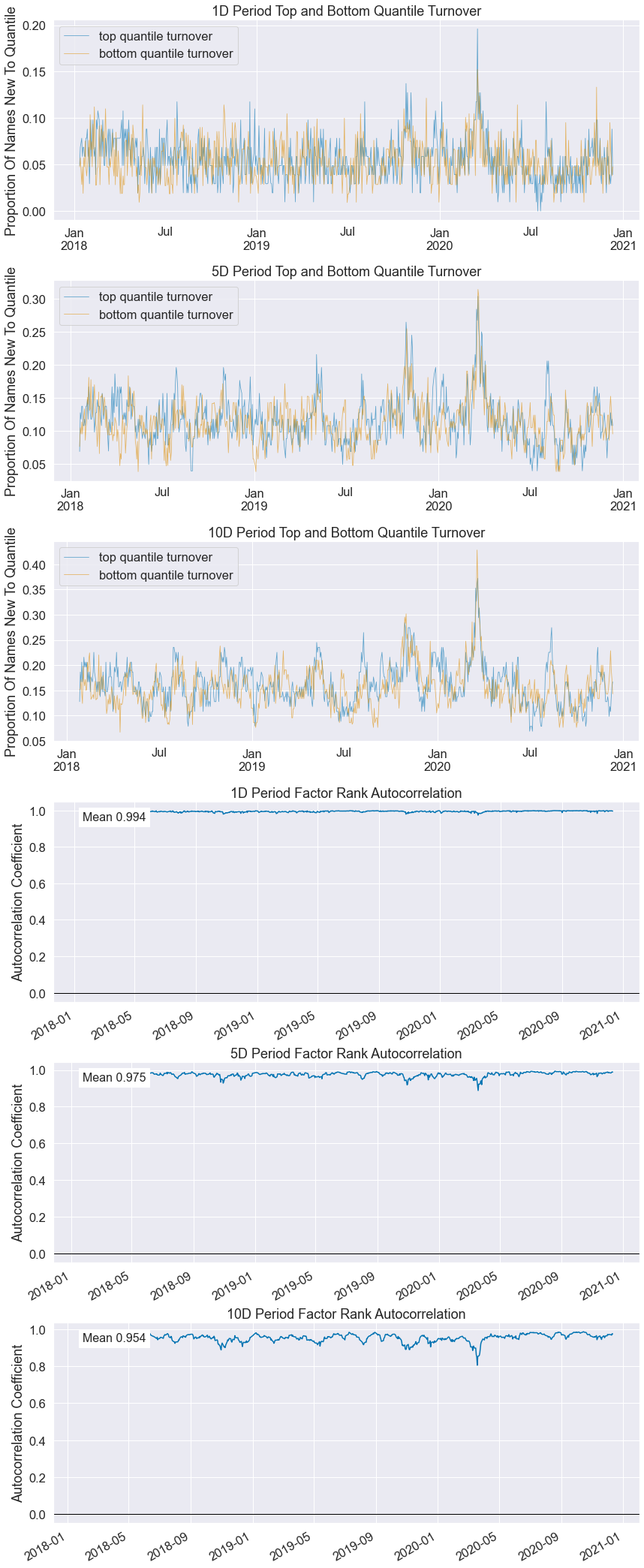

al.tears.create_full_tear_sheet(factor_data, long_short=True, group_neutral=False, by_group=True)

Quantiles Statistics

| min | max | mean | std | count | count % | |

|---|---|---|---|---|---|---|

| factor_quantile | ||||||

| 1 | -0.882437 | 0.336851 | -0.221892 | 0.173761 | 77857 | 20.919291 |

| 2 | -0.788964 | 0.440738 | -0.049322 | 0.143953 | 74322 | 19.969477 |

| 3 | -0.671378 | 0.560727 | 0.058053 | 0.144160 | 70527 | 18.949804 |

| 4 | -0.570969 | 0.765367 | 0.176418 | 0.153070 | 74354 | 19.978075 |

| 5 | -0.463738 | 9.102661 | 0.436519 | 0.325251 | 75118 | 20.183353 |

Returns Analysis

| 1D | 5D | 10D | |

|---|---|---|---|

| Ann. alpha | 0.012 | 0.007 | 0.008 |

| beta | -0.236 | -0.309 | -0.262 |

| Mean Period Wise Return Top Quantile (bps) | -0.345 | -0.764 | -0.528 |

| Mean Period Wise Return Bottom Quantile (bps) | 3.034 | 2.960 | 2.288 |

| Mean Period Wise Spread (bps) | -3.380 | -3.663 | -2.783 |

<Figure size 432x288 with 0 Axes>

Information Analysis

| 1D | 5D | 10D | |

|---|---|---|---|

| IC Mean | 0.017 | 0.017 | 0.010 |

| IC Std. | 0.274 | 0.279 | 0.272 |

| Risk-Adjusted IC | 0.061 | 0.060 | 0.036 |

| t-stat(IC) | 1.648 | 1.640 | 0.970 |

| p-value(IC) | 0.100 | 0.101 | 0.332 |

| IC Skew | -0.228 | -0.323 | -0.357 |

| IC Kurtosis | -0.256 | -0.193 | -0.076 |

Turnover Analysis

| 1D | 5D | 10D | |

|---|---|---|---|

| Quantile 1 Mean Turnover | 0.054 | 0.113 | 0.155 |

| Quantile 2 Mean Turnover | 0.132 | 0.267 | 0.354 |

| Quantile 3 Mean Turnover | 0.159 | 0.312 | 0.408 |

| Quantile 4 Mean Turnover | 0.131 | 0.265 | 0.353 |

| Quantile 5 Mean Turnover | 0.056 | 0.117 | 0.162 |

| 1D | 5D | 10D | |

|---|---|---|---|

| Mean Factor Rank Autocorrelation | 0.994 | 0.975 | 0.954 |

These reports are also available¶

al.tears.create_returns_tear_sheet(factor_data,

long_short=True,

group_neutral=False,

by_group=False)

al.tears.create_information_tear_sheet(factor_data,

group_neutral=False,

by_group=False)

al.tears.create_turnover_tear_sheet(factor_data)

al.tears.create_event_returns_tear_sheet(factor_data, prices,

avgretplot=(5, 15),

long_short=True,

group_neutral=False,

std_bar=True,

by_group=False)

Working with Pyfolio¶

We could use pyfolio to analyze the returns as if it was generated by a backtest, like so

[14]:

pf_returns, pf_positions, pf_benchmark = \

al.performance.create_pyfolio_input(factor_data,

period='1D',

capital=100000,

long_short=True,

group_neutral=False,

equal_weight=True,

quantiles=[1,5],

groups=None,

benchmark_period='1D')

[15]:

import pyfolio as pf

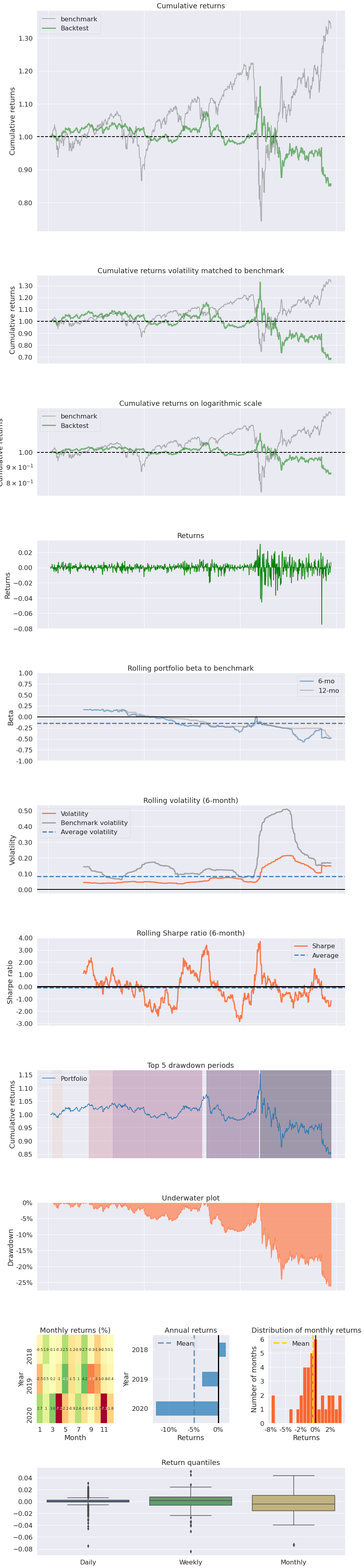

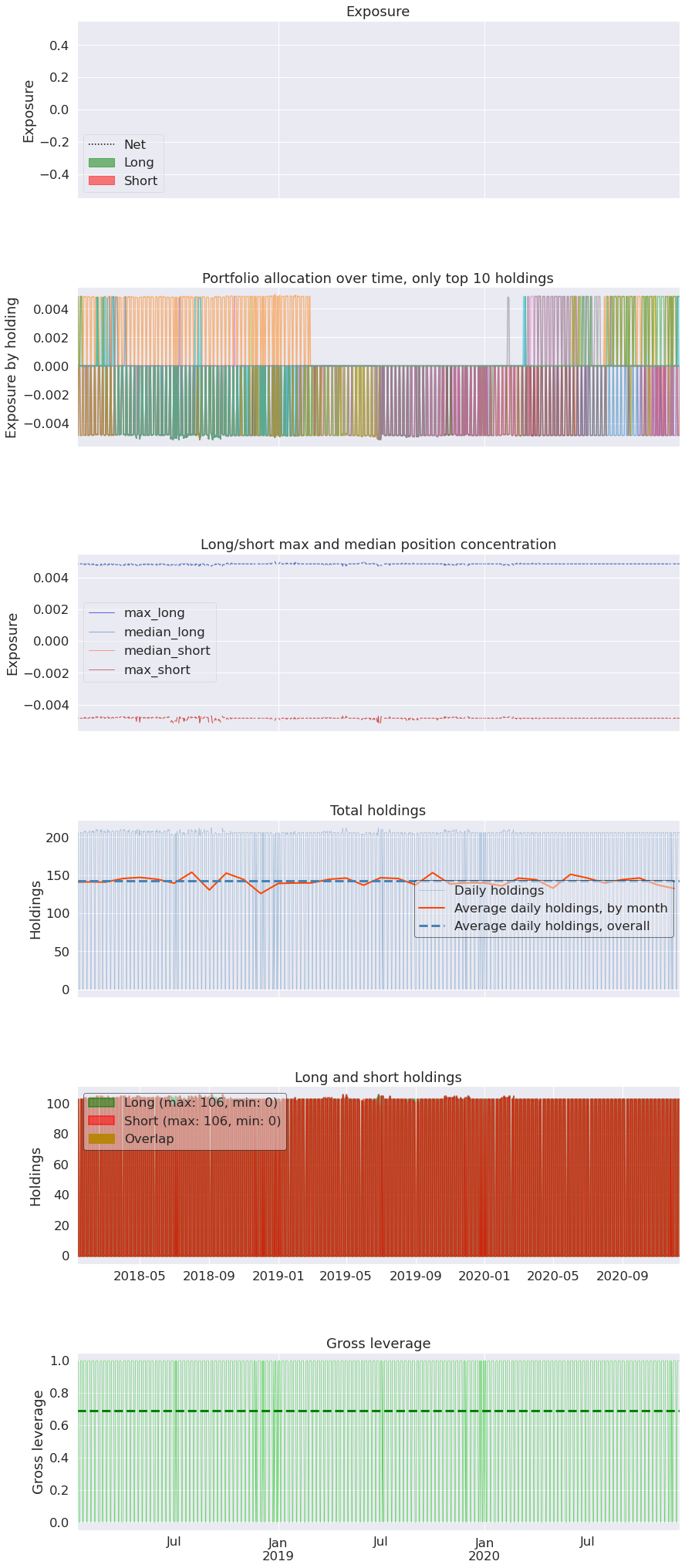

pf.tears.create_full_tear_sheet(pf_returns,

positions=pf_positions,

benchmark_rets=pf_benchmark,

hide_positions=True)

| Start date | 2018-01-10 | |

|---|---|---|

| End date | 2020-12-11 | |

| Total months | 50 | |

| Backtest | ||

| Annual return | -3.584% | |

| Cumulative returns | -14.318% | |

| Annual volatility | 10.102% | |

| Sharpe ratio | -0.31 | |

| Calmar ratio | -0.14 | |

| Stability | 0.36 | |

| Max drawdown | -26.261% | |

| Omega ratio | 0.93 | |

| Sortino ratio | -0.39 | |

| Skew | -2.46 | |

| Kurtosis | 25.59 | |

| Tail ratio | 0.84 | |

| Daily value at risk | -1.285% | |

| Gross leverage | 0.69 | |

| Alpha | -0.01 | |

| Beta | -0.23 | |

| Worst drawdown periods | Net drawdown in % | Peak date | Valley date | Recovery date | Duration |

|---|---|---|---|---|---|

| 0 | 26.26 | 2020-03-17 | 2020-12-09 | NaT | NaN |

| 1 | 9.46 | 2019-08-26 | 2019-11-04 | 2020-03-11 | 143 |

| 2 | 5.86 | 2018-09-03 | 2019-04-17 | 2019-08-08 | 244 |

| 3 | 2.92 | 2018-06-04 | 2018-07-30 | 2018-08-31 | 65 |

| 4 | 1.90 | 2018-01-18 | 2018-02-07 | 2018-02-22 | 26 |

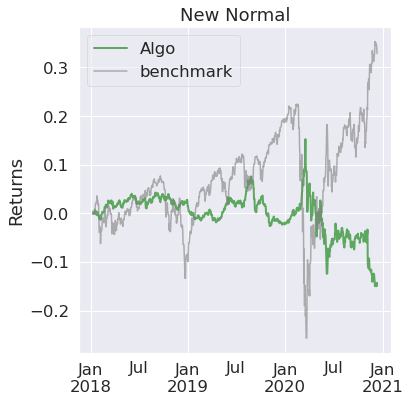

| Stress Events | mean | min | max |

|---|---|---|---|

| New Normal | -0.01% | -7.48% | 3.07% |